Bond veteran Greg Wilensky has seen hype about a surge in inflation crushed too many times to get carried away with this year’s great reflation trade.

“I’ve been managing bond portfolios for 25 years, through very large monetary programs, big deficits, and the Fed trying to raise inflation expectations,” the Janus Henderson money manager said in an interview. “As much as I can see legitimate reasons why it might happen this time – I could have said that very often over the last 12 years too.”

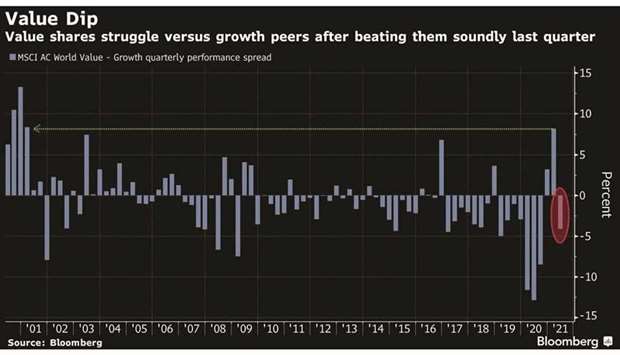

Wilensky’s scepticism epitomises the cooling investor enthusiasm for bets linked to a rapid economic recovery and higher prices. Trades favouring economically-sensitive value stocks, steeper yield curves and a rebound in commodities have faltered after a stellar first quarter.

The MSCI AC World Value Index has lagged its growth counterpart by about 6 percentage points since March 8. Benchmark Treasury yields have retreated some 13 basis points already this quarter, even as US inflation data begin to beat expectations.

And Tuesday’s strong 30-year Treasury auction suggested demand for even the most interest rate-exposed bonds is returning.

One of the biggest questions money managers confront now is whether the stimulus-fuelled rebound in growth and inflation – in particular in the US – can transition to a sustainable expansion that will keep pushing equities and bond yields higher. The International Monetary Fund recently upgraded its 2021 global growth forecast to the strongest in four decades, but the outlook beyond that is less clear-cut.

Envisaging a trajectory for price levels beyond this year is even harder for investors given the warping effect of coronavirus shutdowns, temporary supply bottlenecks and base effects from last year’s disinflation. A surge in five-year US breakevens – a gauge of inflation expectations – has petered out since they hit their highest since 2008 in mid-March.

“Inflation and rates, especially as a bond investor right now, is the call that you have to make,” said Elaine Stokes, fixed income portfolio manager at Loomis Sayles. “It’s the make-or-break call of your year.” The response to the stall for many investors has been to pare back some trades geared to the sharpest stage of the economic rebound. Vishal Khanduja, fixed income fund manager at Eaton Vance Management, has halved his portfolio’s overweight in US inflation-linked bonds from the start of the year.

“Inflation expectations were dislocated in 2020” in a “surgical recession,” Khanduja said. “The typical post-recession positioning that you see happen over multiple years is quickly going through the market.”

As for some traditional inflation hedges in the commodities markets, the story is about to get more complicated than the year-to-date rebound in oil and copper prices would suggest. Strategists at the BlackRock Investment Institute anticipate a divergence within the asset class, as factors such as climate risks are more fully captured in pricing.

“The lift for oil from the economic restart is likely to be transitory, while some metals may benefit from structural trends such as the ‘green’ transition for years to come,” a team including Wei Li wrote in a note this week.

Meanwhile, in the bond market, traders are not reacting to signs of inflation as one might expect.

On Tuesday, data showed US consumer prices climbed in March by the most in nearly nine years, yet 10-year Treasury yields fell five basis points to their lowest in three weeks.